Guide to Non-CRS Countries for Offshore Banking in 2026

Sophisticated investors seek low-tax, high-privacy jurisdictions, often using residence permits and real estate for wealth preservation.

Banks asking about your tax residency used to be rare. Now it's the first question on every account application, every wire transfer, every private banking intake form. That shift happened because of one regulation — the Common Reporting Standard — which rewrote what your bank is legally obligated to tell your government about you.

The numbers are not subtle. As of late 2025, 116 jurisdictions automatically exchange financial account data under the OECD's CRS framework. 171 million accounts. €13 trillion tracked and reportable. And since 2009, countries running offshore compliance programs off the back of this data have collectively collected €135 billion in additional tax, interest, and penalties.

The surveillance net is real and it keeps expanding. But it hasn't swallowed everything yet.

A meaningful subset of jurisdictions — some with sophisticated banking systems, some with citizenship-by-investment programs explicitly designed for internationally mobile capital — still sits outside automatic reporting. This article covers which ones are worth your attention in 2026, what's changed recently, and how to build a banking strategy that actually holds up.

What CRS actually does to your bank

Think of CRS as requiring your bank to work two jobs simultaneously. It serves you as a client, and it serves the tax authorities of whatever country you claim as your tax residence. Every year, your bank sends a report to its local tax authority: your name, account balances, interest earned, dividends received, proceeds from asset sales. That local authority then forwards the file to wherever you live.

The data flows without a request, without a court order, without your consent. You don't receive a copy. You won't know if the information was misrouted, mis-categorized, or accessed by someone who shouldn't have it.

The OECD requires participating jurisdictions to maintain confidentiality standards, but with 2,700+ bilateral exchange relationships active, the practical risk of error or breach scales with the number of links in the chain. Luxembourg-based tax advisers noted in their analysis of AEOI that "with each step — financial institution, local authority, foreign authority — comes a risk of a data breach," and that "taxpayer rights might not have been given sufficient consideration" in how the system was designed.

This isn't paranoia. It's a structural critique of a system that was optimized for revenue collection, not for data security or proportionality.

FATCA: why the US is a privacy haven for non-Americans

American citizens face additional complexity through FATCA, passed by Congress in 2010. FATCA requires foreign banks to identify US account holders and report them to the IRS, or face a 30% withholding tax on US-source income. It's a unilateral rule with teeth.

What makes it relevant to non-Americans: the US does not participate in CRS. It has its own system — and it rarely reciprocates. Foreign governments report their US-person account holders to Washington. Washington sends back far less. This asymmetry has made the United States a functional financial privacy jurisdiction for non-US persons, which is precisely why wealth from traditional offshore centers has migrated toward Delaware LLCs, Nevada trusts, and Florida accounts.

If you hold US citizenship, FATCA is a burden. If you don't, the US banking system offers privacy features that virtually no other major economy provides.

CARF: the crypto reporting framework coming in 2027

One gap that sophisticated investors identified early was crypto. CRS was designed around traditional financial accounts — banks, brokers, insurance products. Digital assets sat outside the reporting perimeter.

That perimeter is closing. The OECD's Crypto Asset Reporting Framework, finalized in 2022, extends automatic reporting to crypto exchanges, brokers, and dealers. As of November 2025, 75 jurisdictions have committed to CARF implementation, and 50 have signed the multilateral competent authority agreement. First exchanges are scheduled for 2027.

The EU's version, DAC8, entered transposition by December 31, 2025. European exchanges began collecting CRS-style data on January 1, 2026. If you use a European-regulated exchange, your 2025 transaction history will be reported to your country of tax residence for the first time next year.

Paraguay has not committed to CARF. El Salvador has not either. For crypto-heavy portfolios, this distinction matters as much as the standard CRS question.

Three jurisdictions no longer on the non-CRS list

The original version of this article included Armenia, Georgia, and Thailand as non-CRS banking destinations. That information is now out of date and we've corrected it.

🇦🇲 Armenia signed the CRS multilateral agreement in January 2024 and began first exchanges in September 2025, covering 47 countries initially. Armenian banks now require CRS self-certifications. Refusal results in account denial. Notably, Armenia began exchanging data with Russia on December 31, 2024 — directly affecting the large community of Russian nationals who relocated there after 2022.

🇬🇪 Georgia signed in November 2022 and commenced exchanges in September 2024. The Georgian Tax Code now carries penalties of up to 3,000 GEL per day for financial institutions that fail to comply. Georgia's once-easy account-opening environment now produces CRS-reportable accounts.

🇹🇭 Thailand signed in March 2022, with its royal decree taking effect March 31, 2023, and first exchanges beginning in September 2023. Thai banks now collect self-certifications for all new accounts.

These three jurisdictions offered real advantages that no longer exist in their original form. We've removed them from the main analysis below.

Montenegro: signed but not implemented

🇲🇪 Montenegro is a peculiar case. It signed the CRS agreement in March 2022, but the OECD's 2025 Peer Review rated its domestic legal framework "Not In Place" — one of only four jurisdictions globally with that determination.

In practice, this means Montenegro is not currently exchanging data. Montenegrin banks do not yet operate under CRS reporting obligations. But the direction of travel is fixed. Montenegro is the EU accession frontrunner, with 13 of 33 negotiating chapters provisionally closed and an accession target around 2028. It joined SEPA in November 2024. It already uses the Euro. Full CRS implementation will arrive with EU membership.

For a short-term banking play, Montenegro may still offer some of what it always offered. For a long-term privacy structure, it's a race against EU accession.

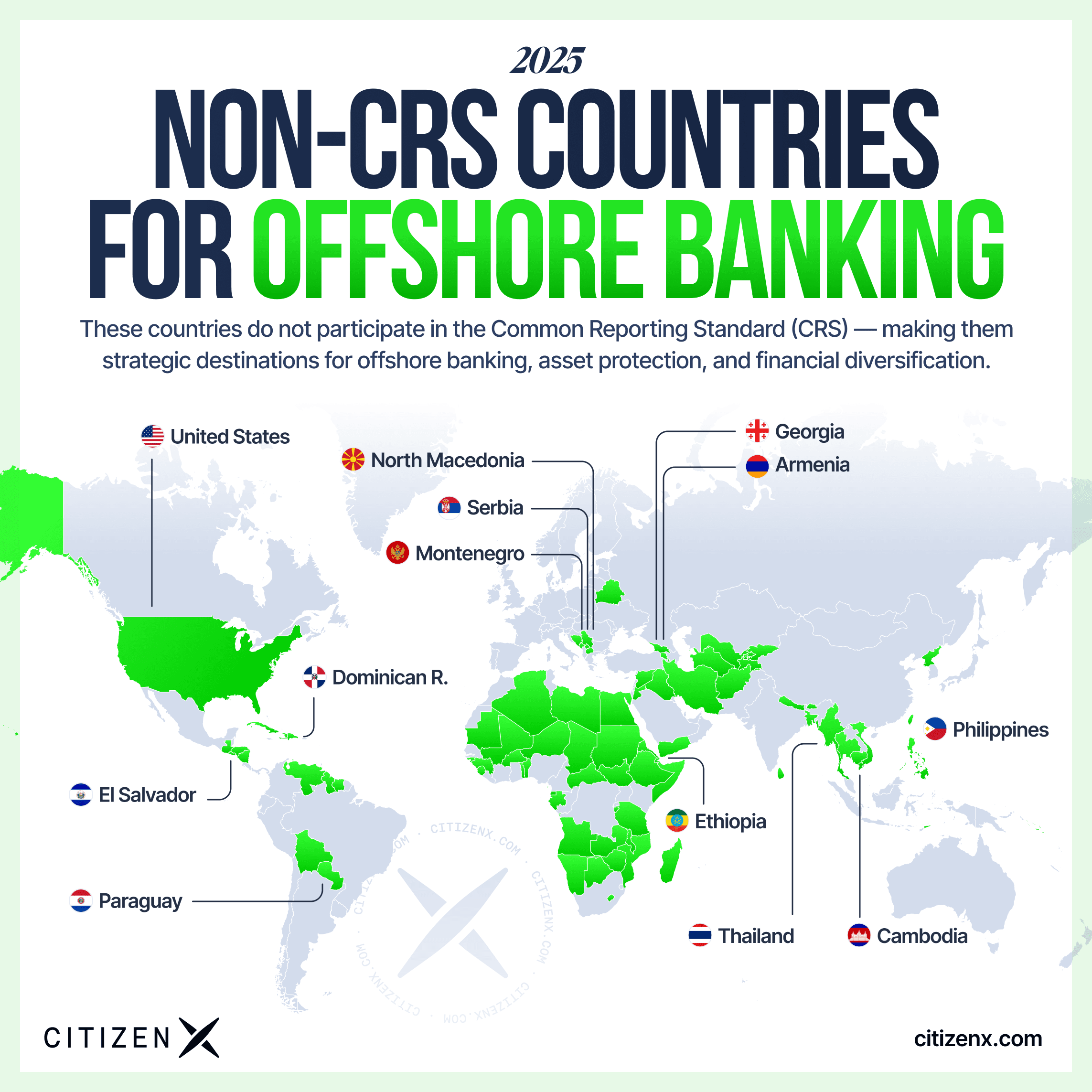

The jurisdictions that still work

What remains after correcting for recent joiners is a smaller, more accurate list. These are confirmed non-CRS jurisdictions with functional banking systems, cross-validated against the OECD's AEOI Commitments document (updated January 12, 2026) and at least two independent sources.

🇸🇻 El Salvador: non-CRS, territorial tax, and zero capital gains on Bitcoin

El Salvador does not participate in CRS. No FATCA agreement with the United States. And in March 2024, its legislature passed Decree No. 969, which explicitly exempted all foreign-source income from taxation — dividends from foreign corporations, capital gains from foreign investments, interest from foreign deposits, repatriation of foreign capital. All of it. This wasn't an interpretation of existing law. It was a deliberate legislative choice to compete for internationally mobile capital.

So what happened to Bitcoin? El Salvador adopted it as legal tender in September 2021. By 2025, actual usage had collapsed — just 8.1% of the population used it regularly, down from 25.7% in 2021. In December 2024, as part of a $1.4 billion IMF facility, Congress revised the Bitcoin Law and made merchant acceptance voluntary. The government wound down the Chivo wallet.

What did not change: zero capital gains tax on Bitcoin. The government continues purchasing BTC — approximately 6,313 BTC as of mid-2025. And El Salvador still accepts Bitcoin as the primary payment method for citizenship.

The Freedom Visa is El Salvador's citizenship-by-investment program, requiring a $1,000,000 non-refundable donation payable in Bitcoin or USDT. The program accepts 1,000 applicants annually, requires no physical residence, processes in approximately 2-4 months, and includes spouses and minor children. Benefits include visa-free access to roughly 130+ countries and the territorial tax regime described above.

New banking guidelines issued February 2025 established a three-tier risk system for foreign investors. Low-risk applicants need only a passport and tax ID to open an account. The system is dollarized — all transactions in USD.

Honest caveat: Freedom House rates El Salvador 47/100 on political freedom, with a 6-point decline in 2024 tied to the ongoing state of emergency. Judicial independence scores poorly. El Salvador is an excellent tax and banking jurisdiction. It is not a model liberal democracy.

For more: El Salvador citizenship by investment →

🇵🇾 Paraguay: territorial tax without automatic reporting — or CARF

Paraguay doesn't participate in CRS, hasn't committed to CARF, and runs one of the simplest territorial tax systems in the world.

Under Law No. 6380/2019, only Paraguayan-source income is taxable. Foreign-source income is fully exempt for individuals and corporations. No wealth tax. No inheritance tax. No capital gains tax on foreign assets. No controlled foreign corporation rules. The corporate rate is a flat 10% on domestic profits. Personal income tax runs 8-10% on services, with exemption thresholds that effectively exempt most expats living off foreign income.

The banking system is stable. The IMF's June 2024 Article IV consultation described it as "stable and profitable," with GDP growth projected at 4.4% for 2025 and inflation near the central bank's 4% target. Paraguay holds approximately 3.9% of global Bitcoin hashrate — mining powered by cheap hydroelectricity from the Itaipú and Yacyretá dams.

Paraguay joined the OECD's Global Forum on tax transparency in June 2016, but only for exchange of information on request — not automatic exchange. Requests require a specific reason. No fishing expeditions.

What to watch: the OECD considers Paraguay a "jurisdiction of relevance" for CRS adoption. GAFILAT's 2022 mutual evaluation flagged persistent AML weaknesses. Money laundering penalties remain capped at 5 years. Paraguay's lack of comprehensive data protection law is a structural gap.

But as of early 2026, Paraguay's account information does not flow automatically to any other government. That is a concrete, verifiable fact about a jurisdiction with a legitimate, low-tax economy.

For more: Paraguay citizenship →

🇵🇭 Philippines: non-CRS in a major economy

The Philippines is one of the most underappreciated banking destinations in the world for privacy-conscious investors, precisely because it's a real country with a real economy — not a micro-jurisdiction dependent on its offshore reputation.

The Philippines does not participate in CRS. It is listed in OECD documentation as a "developing country not asked to commit" with no date set for exchange. As of January 2026, Philippine banks report to Philippine authorities only. Your account balance at Metrobank or BDO does not go to your home government.

The banking sector is substantial. Metrobank, BDO, BPI, and Security Bank operate large private banking divisions with English-speaking relationship managers. International banks including HSBC and Citibank maintain significant operations. Digital banking infrastructure has improved considerably since 2020.

Foreign-sourced income is generally not taxed for non-residents. For residents, income from abroad is taxable, but enforcement against foreign-source income is limited and the territorial orientation of the system provides practical protection.

Account opening requirements vary by institution. Most private banks require a passport, proof of address, and an initial deposit — typically $10,000-50,000 for premium services. Processing takes one to two weeks. Some banks accept initial applications remotely, with in-person signing for final documentation.

The Philippines' geographic position offers connectivity throughout Asia. Ninoy Aquino International Airport serves direct routes to Singapore, Hong Kong, Tokyo, Dubai, and Los Angeles.

🇸🇴 Dominican Republic: Caribbean non-CRS with North American banking standards

The Dominican Republic does not participate in CRS and maintains independence from the Caribbean's broader financial transparency pressures, despite proximity to US-influenced financial systems.

Major international banks operate here — Scotiabank has a significant presence, alongside strong domestic institutions like Banco Popular Dominicano and Banco BHD León. The banking system adopted modern AML/CFT frameworks without joining automatic exchange programs.

Foreign-source income faces minimal taxation. There is no wealth tax. Real estate taxes remain among the lowest in the Caribbean basin.

Account opening for foreigners typically requires a passport, local address documentation, and a bank reference letter. Processing runs one to two weeks. The currency is freely convertible; USD accounts are widely available.

Punta Cana International Airport and Santo Domingo's Las Américas airport offer direct service throughout the Americas and to major European hubs.

🇸🇷 Serbia: European non-CRS, without EU obligations

Serbia does not participate in CRS and has not signed the multilateral agreement. Its EU candidacy is real but distant — accession negotiations have been ongoing for a decade without resolution. Twenty-seven banks operate in the market, including large subsidiaries of Banca Intesa and UniCredit alongside regional players.

The tax system offers a flat 15% personal income tax and a 15% corporate rate, with various incentive structures for foreign investors. The Serbian dinar operates under a managed float, but EUR and USD accounts are widely available.

The banking sector's connection to European networks through Italian and Austrian parent companies provides a level of technical infrastructure that smaller non-CRS jurisdictions cannot match. Private banking services in Belgrade have improved considerably since 2019.

For European investors uncomfortable with more exotic jurisdictions, Serbia offers a recognizable legal tradition, functional courts, and non-CRS status within a 2-3 hour flight of most European capitals.

🇲🇰 North Macedonia: low-tax, non-CRS, EU candidate

North Macedonia's flat 10% personal and corporate tax rates are among the lowest in Europe. The country has not joined CRS. Its EU candidacy is active but Chapters related to financial regulation have not been provisionally closed — accession pressure is real but not imminent.

Twelve private banks operate in the country, with 73.4% foreign ownership (primarily Greek, Austrian, and Slovenian banks). North Macedonia joined SEPA in March 2025, improving cross-border payment infrastructure.

The denar maintains informal Euro pegging, providing currency stability. Skopje International Airport connects directly to major European hubs; most capitals are within a 2-3 hour flight.

🇰🇭 Cambodia: Southeast Asia's most accessible banking market

Cambodia's banking system stands out for its accessibility. Account opening at ABA Bank, ACLEDA, or Prince Bank can be completed in one to two days, with minimal documentation and small minimum deposits. The market is naturally dollarized — virtually all commercial transactions occur in USD, which eliminates currency conversion friction.

The National Bank of Cambodia implemented new digital asset regulations in December 2024 and updated capital adequacy requirements. No CRS commitment exists or appears imminent.

Cambodia's corporate tax rate is 20%, with a lower 0% rate for micro-enterprises. There is no capital gains tax, though legislation to introduce one has been discussed. The country maintains limited tax treaties, which has a practical privacy benefit — there is simply less international coordination infrastructure to activate.

🇺🇸 United States: the largest non-CRS banking system in the world

This is the obvious one that gets least discussion. The United States does not participate in CRS. For non-US persons, US banking relationships offer significant privacy — your account information at JPMorgan or Bank of America does not flow automatically to your home government through any multilateral reporting channel.

The US reciprocates FATCA data selectively and incompletely. Foreign governments send comprehensive account data on US citizens to Washington. Washington sends back limited information. The legal infrastructure for fully reciprocal exchange was never built.

Non-resident aliens with properly structured US banking relationships (using W-8BEN forms rather than W-9 forms) can maintain accounts with minimal tax burden on US-source passive income. Delaware LLCs and Nevada corporations provide additional privacy layers for corporate account structures.

The obvious caveat: US banking is increasingly difficult to access for non-residents. Minimum deposits are substantial, compliance requirements are burdensome, and some major institutions have stopped accepting non-resident accounts for routine private banking. The practical accessibility has declined since 2020. For the right client profile, it remains one of the most powerful non-CRS options. For others, the barriers outweigh the benefits.

🇸🇱 Sierra Leone: non-CRS with an active CBI program

Sierra Leone does not participate in CRS. Its GO-FOR-GOLD citizenship-by-investment program, operating under Section 27A of the Citizenship Act 1973, is designed explicitly around this combination.

The standard fast-track naturalization costs $140,000 (all-inclusive for a single applicant). A heritage route for applicants of African descent, confirmed by DNA test, is available at $100,000. Additional dependents cost $10,000 each, with expanded dependent categories introduced in November 2025 (adult children, siblings under 30, and business partners now eligible). Permanent residency is available separately at $65,000 plus one kilogram of gold bullion.

Applications are entirely remote. Processing takes 60-90 days. Dual citizenship is permitted. The program automatically includes company incorporation and a corporate bank account at Sierra Leone Commercial Bank or Access Bank.

The economic context requires transparency. Sierra Leone is a frontier market — 185th of 193 countries on the Human Development Index, with 16% adult banking penetration. The IMF completed its first and second reviews of Sierra Leone's Extended Credit Facility in December 2025, unlocking $78.8 million. GDP grew 3.9% in 2024, and inflation dropped from 46.6% in 2023 to approximately 4.4% by October 2025. International reserves sat at 1.5 months of imports as of September 2025 — thin.

The Sierra Leone CBI is for investors who want a non-CRS passport with ECOWAS access rights, not a primary banking hub. Using it to establish a banking relationship rather than hold significant deposits makes more sense given the system's scale.

For more: Sierra Leone citizenship →

🇸🇹 São Tomé and Príncipe: the newest non-CRS passport

São Tomé and Príncipe does not participate in CRS. Its citizenship-by-investment program, established by Decreto-Lei n.º 07/2025 (published August 1, 2025), is the newest program globally by a meaningful margin. First passports were issued in January 2026.

The investment is a $90,000 non-refundable donation to the National Transformation Fund for a single applicant — $95,000 for a family of two to four, with $5,000 per additional dependent. A $5,000 non-refundable submission fee applies. Processing averages 2.5 months; the fastest case on record was one month.

The program is administered through a public-private partnership with Passport Legacy under a 10-year exclusive agreement, headquartered in Dubai. Of 98 initial applications received, 27 were approved. Approximately 80% came from Germany, India, Russia, China, and Nigeria.

The tax regime applies personal income tax up to 25% and corporate tax at 25%, but non-residents pay tax only on São Tomé-sourced income. No wealth tax, no inheritance tax, no capital gains tax. CBI citizenship does not create tax residency on its own.

The banking system is small — approximately five commercial banks, with Banco Internacional de São Tomé e Príncipe holding roughly 50% of total assets. The dobra is pegged to the Euro at 1 EUR = 24.50 STD. Three banks were declared insolvent between 2016 and 2022. For actual deposit banking, São Tomé is not the destination — but for a non-CRS passport that pairs with UAE or Singapore banking, the math makes sense.

For more: São Tomé and Príncipe citizenship →

How to actually build a non-CRS banking strategy

Picking a non-CRS jurisdiction based on privacy alone is how people end up with bank accounts in countries they've never visited, at institutions with no correspondent banking relationships, holding currencies that depreciate faster than they earn interest.

The right framework works backwards from your actual needs.

What currencies do you operate in? If your income is in USD and your liabilities are in EUR, a dollarized economy (El Salvador, Cambodia, Dominican Republic) simplifies things. If you need GBP or SGD access, the Philippines or Serbia may provide better correspondent banking.

How often can you actually travel there? Some jurisdictions require in-person account opening or periodic visits to maintain account status. Paraguay's account opening is manageable but not remote-friendly at most institutions. Cambodia and El Salvador have become more accessible.

What's your risk tolerance on jurisdiction stability? Cambodia's banking reforms are real but the regulatory environment remains opaque. Serbia's EU path provides a medium-term backstop. El Salvador's political concentration is a genuine risk even as its tax policy is excellent.

How does this fit your passport portfolio? The strongest banking setups pair a strong passport with accounts in non-CRS jurisdictions where that passport provides legitimate ties. An El Salvador Freedom Visa holder banking in El Salvador has a coherent legal relationship with the country. A random account in a jurisdiction you've never lived in or done business with creates questions you'll eventually need to answer.

The most resilient structure usually looks something like this: a primary account in your country of residence for operational needs, a secondary account in a well-regulated financial center (Singapore, UAE, Switzerland) for wealth management, and a third relationship in a non-CRS jurisdiction that aligns with a genuine life or business connection — citizenship, residency, or commercial activity.

Three accounts. Three jurisdictions. Legal everywhere.

The compliance point that cannot be repeated enough

Non-CRS banking is legal. Failing to report these accounts to your home tax authority, if required, is not.

Most developed countries require their citizens and residents to disclose foreign financial accounts above certain thresholds. The US FBAR requirement applies to accounts exceeding $10,000. UK rules require disclosure under HMRC's self-assessment regime. Most EU member states have similar requirements. Switzerland's domestic banking secrecy, often misunderstood, does not protect Swiss account holders from their own country's reporting requirements — it protects against unauthorized foreign access.

The value of non-CRS banking is privacy from automatic information sharing, not exemption from your own legal obligations. These are different things. Working with qualified advisors in your country of residence is not optional.

The future of this landscape

The OECD's direction hasn't changed since 2014. Zero participating jurisdictions in 2014. 116 by 2025. CARF extends the same logic to crypto by 2027. CRS 2.0 amendments, effective with first exchanges in 2027, bring e-money products into scope and tighten due diligence standards.

The EU accession candidates face the clearest timeline. Montenegro, North Macedonia, and Serbia will all require CRS compliance to join the EU. That's not speculation — it's a condition of accession negotiation. The question is only when.

The Philippines, Cambodia, and the Dominican Republic sit in a different category: developing economies the OECD formally classifies as "not asked to commit." That classification isn't permanent, but changing it requires active political will on the OECD's side. The pressure is softer and the timeline is genuinely unclear.

El Salvador and Paraguay are harder to read. Both maintain OECD Global Forum membership for exchange on request. Neither has CRS commitment pressure built into any existing agreement. El Salvador's IMF relationship creates some international scrutiny but CRS adoption was not an IMF conditionality. Paraguay's situation is similar.

The United States is its own category. Remaining outside CRS while administering FATCA is the world's most successful example of "do as I say, not as I do" in international tax policy. Nothing about Washington's political incentives suggests that changes.

The jurisdictions most likely still outside CRS in 2031: the US, Paraguay, the Philippines, Cambodia, the Dominican Republic, Sierra Leone, and São Tomé. That's a workable list. Smaller than it was five years ago, but enough to build a real structure around.

The window isn't closing as fast as the OECD would prefer.

Frequently asked questions about non-CRS banking

Is non-CRS banking legal?

Yes. Banking in a non-CRS jurisdiction is completely legal. The reporting obligation that CRS creates falls on financial institutions in participating countries, not on account holders. What you are required to do is comply with your own country's foreign account disclosure rules — which may require you to report the existence of the account even if the foreign bank doesn't.

Does a residency permit improve banking access in non-CRS countries?

Usually yes. Most non-CRS jurisdictions offer better account terms, lower minimums, and faster processing for residents. Some — like El Salvador — have developed specific banking frameworks for foreign investors that don't require full residency. A second citizenship provides the most durable banking access.

What's the difference between CRS and CARF for crypto holders?

CRS captures traditional financial accounts — bank deposits, custodial accounts, brokerage accounts. CARF captures crypto-asset transactions at regulated exchanges. If your crypto sits in a non-custodial wallet, neither framework currently touches it. If it sits at a regulated exchange in a CARF-committed jurisdiction, it will be reportable from 2027.

Can I open a corporate account in a non-CRS country?

Yes. Most non-CRS jurisdictions accept corporate accounts, often with more rigorous documentation requirements than personal accounts. Source-of-funds documentation, beneficial ownership disclosure, and corporate structure verification are standard even in jurisdictions without automatic reporting obligations.

What minimum deposits should I expect?

It varies substantially. Cambodia and the Dominican Republic allow basic accounts with minimal initial deposits. Premium private banking relationships in the Philippines, Serbia, or Montenegro typically require $25,000-100,000. El Salvador's new tiered framework has reduced minimum requirements for low-risk foreign investors.

Will more countries join CRS?

Almost certainly. The pattern since 2014 has been consistent expansion. The most likely near-term additions are EU accession candidates (Montenegro, North Macedonia, Serbia) and jurisdictions the OECD identifies as "relevant" to CARF but not yet committed. The US remaining outside CRS is the most significant structural anomaly in the system and shows no signs of changing — FATCA serves as Washington's political substitute for multilateral participation.

CitizenX helps internationally mobile individuals structure their passport portfolios and banking relationships across multiple jurisdictions. All banking and tax situations require qualified legal and tax advice in your country of residence. Book a consultation →